Explaining the Labour theory of Value using simple equations

Explaining the Labour theory of Value using simple equations

The equations were corrected over time. The theory holds up

One of the high schools I attended has a motto in Latin that translates to “nothing without work”. Karl Marx, and before him David Ricardo and Adam Smith, theorized about economics as if “nothing without work” had also been their motto. They identified human labour as the essential measure of value in an economic system. It seems straightforward. Nothing exists in an economy without human labour, and the richest countries in their day were characterized by very rapidly increasing productivity. But the labour theory of value became a favorite punching bag for anti-Marxists.[1]

Can’t one reply to the “nothing without work” motto by saying “there is also nothing without energy, or land, or water etc”? Sure, but water and energy did not design economic systems, and our goal is presumably not to ensure that water or energy are happy. If humans designed an economic system for human goals then it is quite rational to center human labour in your theory of value.

There were errors in the way Marx formulated his labour theory of value, but the essence of it holds up.

I will try to illustrate that by using more accessible math than Ian Wright did in his PhD thesis, part of which was posted on RedSails.org. I found it helpful to do that for myself as I grappled with what Wright ( and a few of his key sources, the economists Piero Straffa and Luigi Pasinetti) wrote, and I believe others may also find it useful.

Marx expressed the value of every commodity in terms of labour time as follows

c + v + s

where c is what Marx called “constant capital’ - the labour time required to replace raw materials and maintain machines and tools used up in the production process; v is what Marx called “variable capital” - the labour time workers require to pay for what they buy; s is surplus value: the extra time the workers stay on the job beyond what they need to pay for their own consumption goods.

But capitalism functions using money prices, not labour time. So how do we convert (or “transform” as Marx put it) the labour time values into prices? Marx dealt with this problem in Volume III, Chapter 9 of Das Kapital.

Marx’s transformation as three equations

Pasinetti (who was very sympathetic to Marx and perhaps even a Marxist) explained Marx’s solution by imagining an economy that produces three types of goods:

Goods used by firms for production

Consumer goods bought by workers

Consumer goods bought by capitalists

Three equations would have to hold for the system to be able to sustain itself

Equation 1: c1 + v1 + s1 = c1 + c2 + c3

The value (measured in quantity of socially necessary labour) produced in sector 1 (the production goods sector) must equal the value of “means of production” purchased by firms in all 3 sectors

Equation 2: c2 +s2 +v2 = v1 + 2 + v3

The value produced in sector 2 (the workers’ goods sector) must equal the value of the wage goods purchased by workers in all 3 sectors

Equation 3: c3 + v3 + s3 = s1 + s2 + s3

The value produced in sector 3 (the capitalist consumer goods sector) must equal the value of the consumer goods purchased by capitalists in all 3 sectors

This system of three linear equations describes “simple reproduction” because capitalists simply spend all their surplus value on goods from sector 3. Workers similarly spend all they earn on sector 2.

Crucially, Marx also said that it is only workers on the job today that create surplus value: “the value of the constant capital reappears in the value of the product, but does not enter into the newly produced value” [Das Kapital Vol I, Chapter 11] But if wages are all driven to the same level by competition, and if living labor alone creates surplus value, then it must follow that the ratio of surplus value to wages paid in each sector must also equalize. In mathematical terms using our three sector example, it means that the following should be true

s1/v1 = s2/v2 = s3/v3

But Marx acknowledged that it would not be true - that in a capitalist economy it is profit rates that will tend to be driven to equality through competition, not the surplus value rates. Profit rates would be given by

r = s / (c + v)

Dividing the numerator and denominator on right side by v, we get

r = (s/v) / (c/v + 1)

The only way surplus value rates (s/v) and profit rates r can both be the same in all three sectors is for a special case where

c1/v1 = c2/v2 = c3/v3

So in a capitalist economy, money prices for commodities 1,2 and 3 must (except for a special case) diverge from the labour time values given by Equations 1,2 and 3.

Marx explained this divergence by arguing that the uniform rate of profit, r, that is achieved through competition is the result of capitalists unequally distributing surplus value among themselves. Pasinetti summed it as follows

Equation 4: r = (s1 + s2 + s3) / (c1+c2+c3+v1+v2+v3)

But despite unequal rates of surplus value from one sector to another, Marx argued that in the aggregate (all sectors combined) total profits equal total surplus value. Marx also said that “the sum of the prices of production of all commodities produced in a society…is equal to the sum of their values”. Money and labour time have different units of measure so a proportionality constant, K, is required to relate total price to total labour time. Hence, Marx’s assertion regarding prices and values would actually have to be expressed as follows

p1 = K [c1 + v1 + r (c1 + v1) ]

p2 = K [c2 + v2 + r (c2 + v2) ]

p3 = K [c3 + v3 + r (c3 + v3) ]

But for simplicity assume that we have defined units for time and money such that K is equal to one. In that case the equations become

Equation 1A: p1 = c1 + v1 + r (c1 + v1)

Equation 2A: p2 = c2 + v2 + r (c2 + v2)

Equation 3A: p3 = c3 + v3 + r (c3 + v3)

Note that p1, p2, p3 are not unit prices but the price of everything produced in sectors 1,2 and 3 respectively..Substitute Equation 4 into Equations 1A, 2A and 3A. Then add them up. The result is that

Equation 6: p1 + p2 + p3 = c1 + c2 + c3 + v1 + v2 + v3 + s1 + s2 + s3

The left side is the money price of everything workers produce. The right side is the value of all labour time (converted into money assuming units such that the proportionality constant is equal to 1). Remember that this considers not just the labour time workers in each sector spend on the job but also the labour time that went into making everything the current workers use on the job (i.e direct and indirect labour).

Marx conceded that his procedure for converting labour values to prices might require further adjustments because his procedure does not address all the terms for constant and variable capital that are expressed as values. Marx died without elaborating further.[2]

Enter Ladislaus Bortkiewicz with his equations

In 1907, the Russian economist Ladislaus Bortkiewicz said that the following three equations were what Marx should have used to convert labour values to prices.

Equation 1B:(c1p1 + v1p2)(1+r) = (c1 + c2 + c3)p1

Equation 2B:(c2p1 + v2p2)(1+r) = (v1 + v2 + v3))p2

Equation 3B:(c3p1 + v3p3)(1+r) = (s1 + s2 + s3)p3

where p1,p2, and p3 are money prices of the goods in each sector per unit of labour time. So the first term in Equation 1B, c1p1, is the money value of raw materials in sector 1. The second term, v1p2, is the money value of what workers in sector 1 receive. The entire left side of Equation 1B is the money value of the inputs to sector 1 marked up by the profit rate, r. The right side of Equation 1B is the total labour time output of sector 1 converted into a money value by multiplying it by p1. The other two equations are similarly constructed.

Note how Bortkiewicz converted every term in equations 1B, 2B, and 2C into units of money. This was indisputably an improvement on Marx’s approach..

If all the labour time values are known in Equations 1B, 2B, and 3B then there are four unknowns: p1,p2,p3, and r. Since there are four unknowns but only three equations, one of the unknowns must be chosen to be able to solve for the other three. Bortkiewicz chose to set p3 equal to 1.

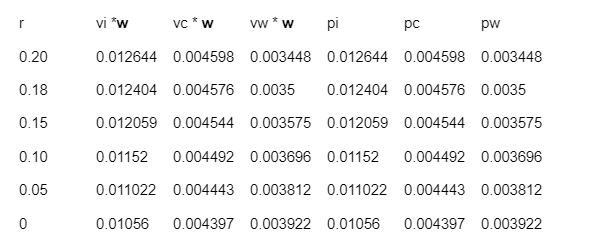

Bortkiewicz then used his solution to provide numerical examples that converted total labour time values into money prices. It did not equal the total price of all production. Below are two of the tables Bortkiewicz presented using his solution.

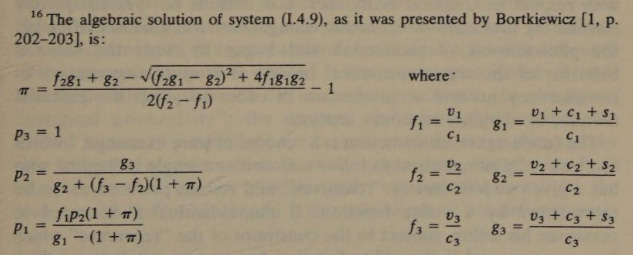

One last thing on Bortkiewicz’s solution that‘s worth nothing. Below are his equations for profit and prices (derived by solving Equations 1B,2B and 3B). Note how complex and interrelated (i.e. tangled up) profits are with prices in his solution. [3]

Enter Sraffa. Does the labor theory of value matter?

As I explained in a previous piece, the economist Piero Sraffa solved a system of three equations and three unknowns that describe simple reproduction but he made no use at all of the labour theory of value. Also, rather than set one of the prices equal to an arbitrarily chosen number in order to solve them (like Bortkieeicz did by setting p3 equal to 1) Sraffa set prices relative to a “standard commodity”: a combination of the three commodities with mathematical properties that it is always possible to extract from a system of linear equations that describe simple reproduction.

By doing that, Sraffa showed that there is always a direct trade off between the profit rate ( r ) and wages given by the simple formula

w = 1 - r/R

where w is the share of national income that goes to workers and R is the maximum attainable profit rate. When r is equal to R, w is zero.

Thanks to Sraffa, nobody could claim the distribution of income under capitalism involved some complicated relationship with prices; or deny the directly conflicting interests of workers and capitalists - all without any need to defend the labour theory of value. But Sraffa could have gone further.

Enter Ian Wright with total labour costs

All capitalists (and apologists for capitalism) see the capital class as inevitable - as if wishing for it to be abolished is like wishing for the abolishment of all government and all laws. But communists should see the capitalist class as an unnecessary cost. Capitalists can’t consume unless workers produce what they buy. That’s the insight that Wright relies on to further correct the labour theory of value.[4]

Let’s recall the example that Piero Sraffa used of linear equations that defined a simple reproduction economy that produces three goods. The fourth equation below is the net national income set equal to 1:

Equation 1C: (90pi + 120pc + 60pw)(1+r) + 3/16w = 180pi

Equation 2C:(50pi + 125pc + 150pw)(1+r) + 5/16w = 450pc

Equation 3C: (40pi + 40pc +200pw)(1+r) + 8/16w=480pw

Equation 4C: 165pc + 70pw = 1

where

pi = unit price of iron

pc= unit price of corn

pw= unit price of wheat

r = profit rate

w= wages (more specifically, the share of the national income that goes to workers).

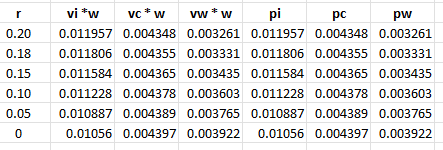

For the equations above, another system of equations relates what Wright defines as super-integrated labour values, vi, vc and vw. These values include the direct and indirect labour time that produces everything capitalists buy. Note that there are no money terms in the three equations below.

Equation 5c: vi = ( (90/180)vi + (120/180)vc + (60/180)vw ) (1+r) + 3/16

Equation 6c: vc = ( (90/180)vi + (120/180)vc + (60/180)vw ) (1+r) + 5/16

Equation 7c: vw = ( (90/180)vi + (120/180)vc + (60/180)vw ) (1+r) + 8/16

If we pick a value for r, we can solve equations 1C, 2C and 3C to get pi,pc, pw and w. We can also solve equations 5C, 6C, and 7C to get vi, vc and vw.

The table below shows the solutions for various values of r. [5]

The important thing to observe in the table is that for every value of r the price of each commodity is equal to its super-integrated labour value multiplied by w

pi= vi * w,

pc = vc * w,

pw = vw *w

Multiply each equation by the quantity of each commodity that is produced: Qi, Qc, Qw. Then add the equations together and you get

Qipi + Qcpc + Qwpw = [Qivi + Qcvc + Qwvw] w

This equation states that the money value of of commodities workers produce ( the left side) is equal to the money value of their labour time.(the right side).

In his thesis, Wright cautions that a general labour theory of value “is merely one of many real cost theories that differ in their choice of measuring unit, such as a general corn theory of value, a general energy theory of value etc….”

But if humans vanished from the world none of the other inputs could create value: not unless another species eventually emerged that debated about economic systems.

NOTES:

[1} Influential economist Paul Samuelson rubbished the theory to dismiss Marx but, for reasons we can guess, spared pro-capitalist Ricardo and Smith. In one paper, Samuleson used his attack on the labour theory of value to dismiss volumes I and II of Das Kapital a “muddle” but still praised Ricardo as “clever”.

In that paper, Samuelson also dismissed Marx’s theory of exploitation by equating it to rightwing libertarians saying that people only work for themselves once their tax bill is paid. But governments are inevitable and necessary. Capitalists are not

[2] In fact Volumes II and III were published posthumously.

[3] I am using Pasinetti’s presentation of Bortkiewic z solution (on page 23) to keep consistency in the naming of variables.

[4] Marx didn’t believe that capitalism was inevitable, so how did he miss that point? Wright says that “Marx, unfortunately, attempts to explain a factual cost structure that includes surplus-value as a cost, that is natural prices, in terms of a counterfactual cost structure that excludes surpluslabour as a cost, that is classical labour costs”. Capitalists should not exist but do, and the costs of mainataining them must be accounted for as a real cost.

[5] A very similar table is obtained if instead of setting national income equal to one in Equation 4c, Sraffa’s standard commodity is used. In this numercal example that would mean that Equation 4C becomes

40pi + 60pc + 80pw = 1

This is the table that is obtained